Clear Categories

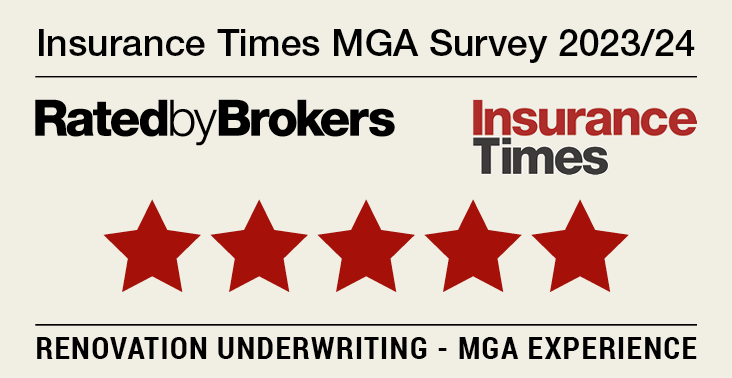

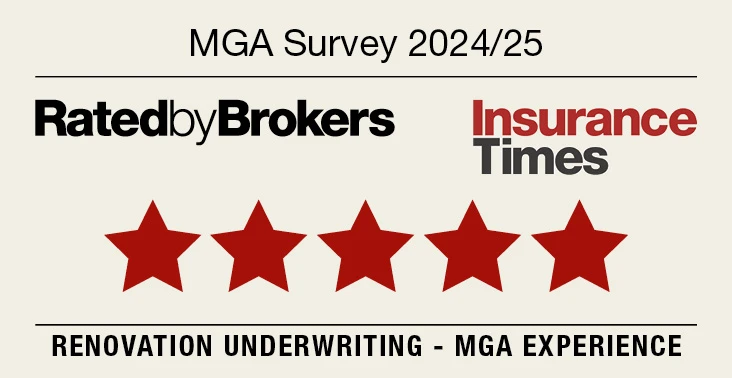

Results

There’s a lot to say about renovation insurance, and we’re proud to be experts on the subject. We share all our company news here. Choose whether to scroll through, or use the filters to tailor the content for your area of interest